The following are eligible for filing Form ITR-5:

It is pertinent to mention that a person who is required to file return of income under Section 139(4A) or 139(4B) or 139(4D) cannot use Form ITR-5 for filing return.

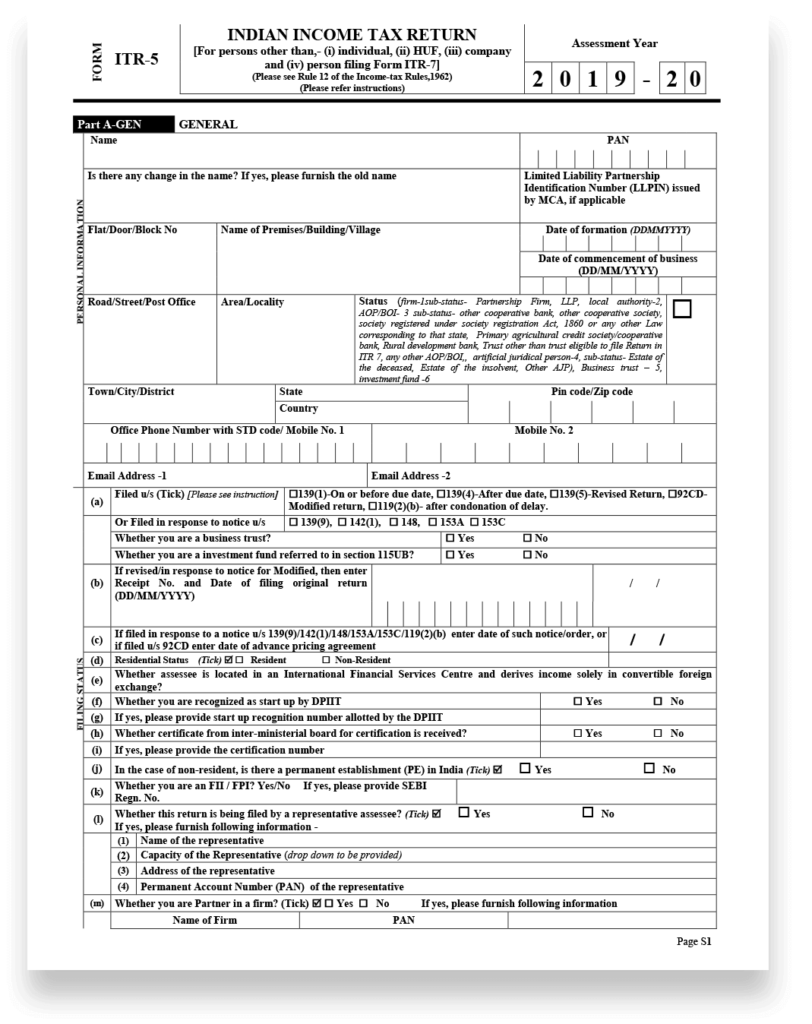

Form ITR-5 is an elaborate form that has primarily two parts. There are also multiple schedules in the Form:

| Part/Schedule | Explanation |

|---|---|

| Part A-GEN | General information |

| Part A-BS | Balance sheet as on the last day of the previous year |

| Part A – Manufacturing Account | Manufacturing Account for the previous financial year |

| Part A – Trading Account | Trading Account for the previous financial year |

| Part A – P&L | Profit and Loss for the previous financial year |

| Part A – OI | Other Information (this is optional in case the assessee is not liable for audit under Section 44AB) |

| Part A – QD | Quantitative Details (this is optional in case the assessee is not liable for audit under Section 44AB) |

| Schedule- HP | Income computation under the head House Property |

| Schedule – BP | Income computation under the head – Business or Profession |

| Schedule DPM | Computing depreciation on Plant & Machinery in accordance with the Income Tax Act |

| Schedule DOA | Computation of Depreciation on other assets as per the Income Tax Act |

| Schedule DEP | Summary of depreciation on all assets as per the Income Tax Act |

| Schedule DCG | Computing of deemed capital gains on the sale of depreciable assets |

| Schedule ESR | Making deduction under Section 35 |

| Schedule- CG | Computing income under the head Capital Gains |

| Schedule- OS | Computing income under the heading Income from other sources |

| Schedule CYLA | Income statement after setting-off losses for the current year |

| Schedule BFLA | Income statement after setting off the unabsorbed losses of the previous year(s) |

| Schedule CFL | Statement of losses which is to be carried forward to the future years |

| Schedule UD | Statement regarding unabsorbed depreciation |

| Schedule ICDS | |

| Schedule 10AA | Computing the deduction under Section 10AA |

| Schedule 80G | Statement pertaining to donations which are entitled for deduction under Section 80G |

| Schedule RA | Statement of donations made to research associations etc. which are entitled for deduction under Sections 35(1)(ii), 35(1)(iia), 35(1)(iii) or 35(2AA) |

| Schedule 80IA | Computing deduction to be made under Section 80IA |

| Schedule 80IB | Computing deduction under Section 80IB |

| Schedule 80IC/80IE | Computing deduction under Section 80IC/80IE |

| Schedule 80P | Deductions under Section 80P |

| Schedule VIA | Deductions statement under Chapter VIA |

| Schedule AMT | Computing Alternate Minimum Tax under Section 115JC of the Income Tax Act |

| Schedule AMTC | Calculation of tax credit under Section 115JD |

| Schedule SPI | Statement of income that arises to minor child/spouse/son’s wife or any other person or AOP that is to be included in the income of the assessee in Schedules HP, CG, OS |

| Schedule SI | Statement of income which is subject to chargeability at special tax rates |

| Schedule IF | Details of partnership firms in which assessee is partner |

| Schedule EI | Exempt Income Details |

| Schedule PTI | Details of pass through income from investment fund or business trust under Section 115UA, 115UB |

| Schedule FSI | Details of income that accrues or arises out of India |

| Schedule TR | Details of any taxes that have been paid outside India |

| Schedule FA | Details of any Foreign assets or income from a source outside India |

| Schedule GST | Details of turnover/gross receipts reported for GST |

| Part B-TI | Summary of total income and tax computation on the basis of the income that is chargeable to tax |

| Part B – TTI | Computing the tax liability on total income |

| Tax Payments | Advance Tax, Tax Deducted at Source and Self-assessment tax |

The audit report can be generated online while filing the return. For this click on Audit Report, then 3CA-3CD and finally on generate report.

Form ITR 5 cannot be filed by individual taxpayers, HUF, Company, Persons who have to file tax return in Form ITR-7, i.e., under Sections 139(4A), 139(4B), 139(4C), 139(4D), 139(4E) or 139(4F).

ITR-5 must be filed by firms, LLPs (Limited Liability Partnerships), AOPs (Association of persons) and BOIs (Body of Individuals), artificial juridical person, cooperative society and local authority.